Reviewing the 2018 Accounting Standards

- Practitioners now are part of every peer review visit team.

- Almost 96 percent of host schools were satisfied with the performance of the practitioners.

- As more schools seek accounting accreditation, more qualified practitioners will need to be found and trained.

AACSB passed new accounting standards in 2018. In the three years since we began implementing those new standards, we’ve learned a great deal. Some things have worked well, but we are always contemplating how we can do even better. An overarching goal continues to be bridging the gap between academia and practice.

The new standards were accompanied by several innovations. For instance, we formed an Accounting Accreditation Policy Committee (AAPC) and populated it with accounting program leaders and accounting practitioners. We streamlined the accounting standards to eliminate redundancy of reporting between business and accounting peer review teams. And we placed a greater emphasis on technology as an integral component of the accounting curriculum.

But arguably the most innovative change we made with the 2018 standards was incorporating practitioners into the accounting accreditation process—at every level.

Practitioners Play a Major Part

Practitioners now play key roles in three areas of AACSB accreditation:

Peer review teams. Our first step was to add accounting practitioners to all accounting peer review visit teams. This innovation was implemented because the Accounting Accreditation Task Force believed practitioners were uniquely positioned to evaluate programs by how well they did three things: displayed currency and relevance; integrated with the profession; and infused technology throughout the curriculum, rather than embedding it in one course. Today, accounting practitioners play an integral role on every team, and their role will become even more important in the future.

The Accounting Accreditation Policy Committee. Since the AAPC oversees changes to the standards and guidance related to the standards, adding practitioners to this committee means that industry professionals now have a voice in how guidance evolves to support the standards. Per AACSB’s governance guidelines, the number of academics and practitioners are in roughly equal proportion on the AAPC. Currently, five of the 11 seats are held by accounting practitioners, all of them individuals who have participated in accounting accreditation visits and are highly experienced in public or private accounting practice. One seat is held by a board member, who maintains a connection between the committee and the AACSB board of directors.

The Accounting Accreditation Committee. To ensure that the accounting standards are applied fairly and consistently, the AAC oversees accounting accreditation peer review team visits for schools seeking initial accreditation as well as those undergoing continuous improvement review (CIR).

Feedback Shows High Approval

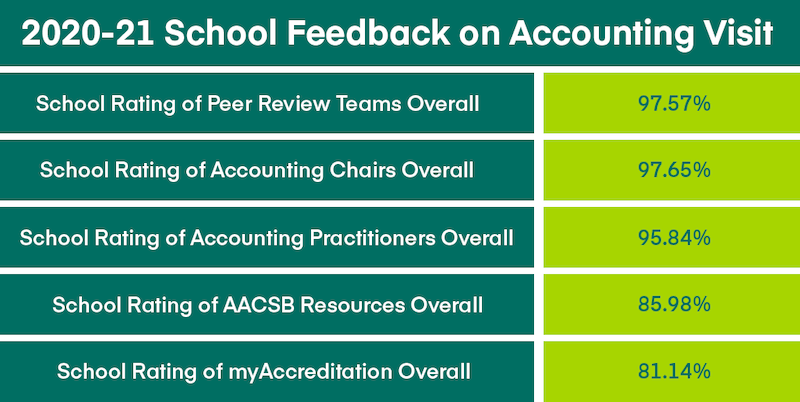

The addition of practitioners to the accounting accreditation process has received high marks from member schools. To gauge member satisfaction, AACSB collects feedback from host schools through post-visit surveys. Our goal is to receive ratings of 85 percent or better in all the areas we measure.

Feedback from the 2020–21 surveys shows that almost 96 percent of respondents were satisfied with the performance of the practitioners on the teams. School representatives said they found value in getting the practitioner’s perspective on the curriculum and receiving input on the technology aspect of accounting degree programs.

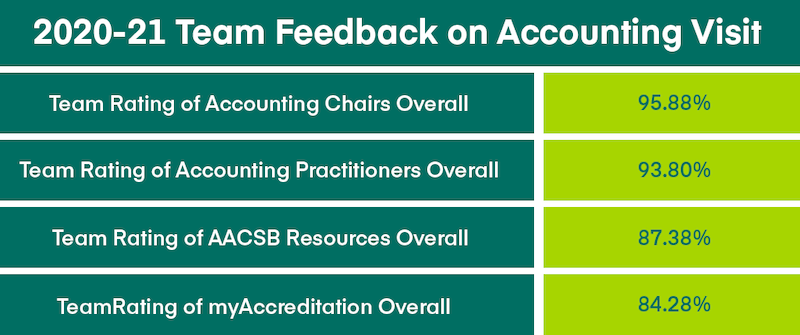

In addition to collecting feedback from the host schools, AACSB solicits feedback from peer review teams. In 2020–21, almost 94 percent of respondents said they were satisfied with the performance of the practitioner on the team. Comments from team members echoed the sentiments expressed by host schools, so we know that the addition of practitioners has been well-received overall by both groups.

In fact, the surveys show that there is only one area of the accounting visits where AACSB is not achieving its target of 85 percent satisfaction, and that’s myAccreditation. We launched myAccreditation in 2020–21, and while the rollout went smoothly overall, there has been a learning curve among our schools and volunteers. We are continuing to make enhancements that improve the usability of the system.

More Practitioners Are Needed

While these data tell us the practitioner model is working, integrating industry professionals into the accreditation process has presented some challenges. The biggest one is finding enough trained practitioners to serve on the teams.

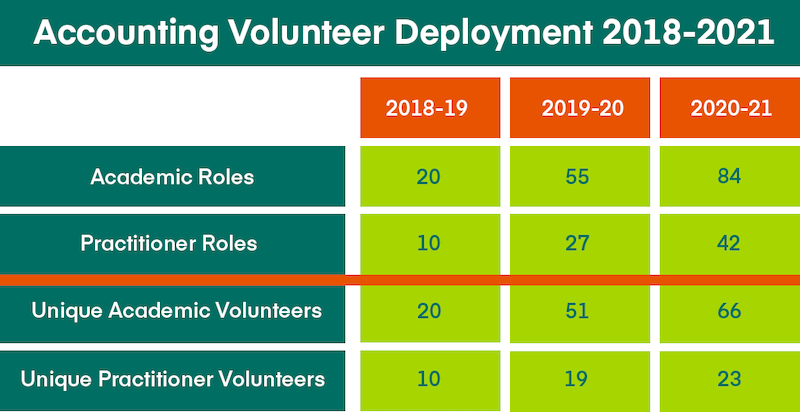

Because the new standards were gradually phased in, the problem was not evident right away. During the pilot phase in 2018–19, only 10 schools in the CIR process were evaluated under the new standards, and during the optional phase in 2019–20, only 23 schools undergoing CIR and one school pursuing initial accounting accreditation were evaluated with the new standards. But by 2020–21, when the new standards were required, we needed volunteers to work with 45 CIR schools and one initial school that were evaluated under the new standards.

Integrating industry professionals into the accreditation process has presented some challenges. The biggest one is finding enough trained practitioners to serve on the teams.At the close of the 2020–21 academic year, a total of 80 schools had gone through an accounting visit under the 2018 accounting standards. In keeping with the geographic distribution of the Accounting Accreditation Council, most of these schools were in the Americas; two were from the EMEA region, and three were from the AP region.

During those three years, 154 individuals served on accounting review teams. The chart below shows how these volunteers were deployed. Figures for academic and practitioner roles represent the number of positions that needed to be filled on peer review teams, while figures for volunteers represent the number of actual people who filled those positions every year.

What’s quickly clear is that, as the new standards became more widely adopted, we didn’t have as many individuals as we needed to serve on the peer review teams. By 2020–21, we needed almost 20 more academics and 20 more practitioners than we had available. Therefore, we had to ask practitioners to do more than one visit within a single season, which is outside of our normal protocols. The following year, we also had to ask practitioners to serve on more than one team.

To ensure our team model is sustainable over the long run, we must continue to expand the practitioner pool. Currently, there are 31 trained practitioners in our volunteer base; we would like to increase that number to 75 within the next three to five years. We will need to increase our number of accounting practitioners even more if we achieve our goal of spurring significant growth in the number of schools that pursue accounting accreditation. We can do it—but it will take work.

A Search for More Practitioners

When we launched the new standards, we recruited practitioners through a partnership with the American Institute of Certified Public Accountants (AICPA). Today, we actively seek referrals from AACSB volunteers. We are also considering other methods of publicizing this opportunity, as practitioners tell us they have enjoyed the experience of connecting back to academia. For instance, we might ask for referrals from practitioners, our board of directors, our Business Practices Council, and groups such as the Institute of Management Accountants and the AICPA.

Practitioners suitable for peer review team service must meet three criteria.

They must have work profiles that include:

- Current experience as practicing accountants with at least 10 years of full-time professional accounting experience.

- Strong written and oral communication skills.

- Strong emotional intelligence.

They must meet at least one of three experience requirements:

- Service on peer review teams at accounting firms.

- Service on a university’s accounting advisory council or board.

- University teaching experience and/or an understanding of university processes and governance.

They must possess three competencies essential to this role:

- Strong knowledge of and facility with current technology.

- Ability to assess an accounting curriculum to determine whether it is sufficiently current, relevant, and timely to meet the workforce needs of today’s graduates.

- Ability to evaluate whether the school is using and teaching current and emerging technologies appropriately within the accounting curriculum.

In addition, practitioners must not have a conflict of interest with the schools where they are conducting evaluations. To provide quality control in this area, AACSB requires an annual conflict of interest attestation.

Once they are selected to serve on teams, accounting practitioners participate in the same training as all other business and accounting volunteers; they also participate in online training geared specifically to their particular role.

Accounting program leaders who would like more information about accounting practitioner service can email Maria Baltar at [email protected].

What’s Next

In addition to recruiting more practitioners to serve on accounting review teams, we are considering revamping the team model. Currently, schools seeking supplemental accounting accreditation along with regular business accreditation are visited by five-member teams that consist of two academics plus a practitioner for the accounting accreditation and two academics for the business accreditation (a 3+2 model).

Some peer review team members and host schools have remarked on the imbalance of having three team members dedicated to one discipline and only two members dedicated to the entire rest of the business school. For that reason, for 2022–23 visits we are experimenting with a 2+2 model that will consist of two business members, one accounting academic, and one accounting practitioner. We would still have the option of bringing in a fifth member who could be either a business member or an accounting academic. A fifth member, who would be added at the discretion of AACSB or at the request of the school, would be most appropriate if the business school is mid-sized or large, has complex operations, or is spread over multiple campuses.

We are experimenting with a 2+2 model that will consist of two business members, one accounting academic, and one accounting practitioner.

Fifth team members also could be added if the team includes a new dean or accounting program head making his or her first visit. Since we like to pair experienced and inexperienced volunteers, there will be times when a new leader would need an experienced team member to guide the visit. We will evaluate how well this model holds up and—as always, in the spirit of continuous improvement—adjust if needed.

Like our member schools, AACSB embraces the need to evaluate, experiment, and improve on an ongoing basis. We always value receiving the thoughts and perspectives of our members. As the old African proverb says, “Alone we move fast, but together we move far.”